The economic impact of climate change is becoming increasingly urgent as new studies reveal projections six times greater than previous estimates. As global temperatures rise, experts warn of significant repercussions, including a staggering 12 percent decline in global GDP for every additional 1°C increase. This alarming trend is attributed to a diverse range of economic factors, including the increased frequency of extreme weather events and their detrimental effects on productivity. With climate change projections indicating escalating risks, the economic toll of climate change poses challenges that demand immediate action. To mitigate these risks, effective decarbonization policy must prioritize the economic ramifications and strive to lower the long-term costs of carbon emissions.

The ramifications of climate-related shifts on the economy are drawing critical attention, as researchers forecast dire outcomes that could reshape global financial landscapes. Current analyses suggest that the deterioration of economic health, linked to global temperature surges, may result in a drastic contraction of the Gross Domestic Product across nations. Moreover, as we witness a rising tide of extreme weather phenomena, the pressing need to address the financial consequences of environmental degradation cannot be overlooked. This situation calls for strategic policy responses that emphasize reducing carbon footprints at a national and global level, pointing to the importance of sustainable practices to avert an inevitable economic downturn.

The Rising Economic Toll of Climate Change

Climate change is poised to have an increasingly severe impact on the global economy, with projections indicating that each additional 1°C rise in temperature could lead to a 12 percent decline in global GDP. This stark prediction is much larger than earlier estimates and demonstrates an urgent need for economies to adapt to these shifts. The economic toll of climate change not only encompasses reduced productivity but also considers the ramifications of extreme weather events that are becoming more frequent due to increasing global temperatures.

Furthermore, as researchers have noted, the complexities of estimating the economic fallout from climate change are multilayered. While traditional economic indicators such as GDP growth may suggest that economies are robust, the underlying reality shows that unchecked warming could drastically alter consumption and production patterns on a global scale. The long-term projections raise critical questions about the adaptability of current economic models, as they may not fully account for the inevitable effects of a warming world.

Understanding Climate Change Projections

Accurate estimates and projections regarding climate change are crucial for policymakers and economists alike. Recent studies reveal that the traditional models previously used may underestimate the potential declines in economic productivity due to climate change. Specifically, researchers Adrien Bilal and Diego R. Känzig emphasize that utilizing a global temperature variable—reflective of the current geoscientific understandings—can provide a more reliable basis for projecting economic impacts. This shift in methodology is essential for aligning economic forecasts with reality.

The implications of these revised climate change projections are significant, particularly as they relate to fiscal planning and resource allocation for countries worldwide. By understanding that continued warming could lead to a 50 percent decline in output and consumption by the century’s end, governments can better prepare and implement strategies to mitigate these potential losses. Such strategies should align closely with decarbonization policies aimed at reducing emissions and ultimately safeguarding economic stability.

The Global GDP Decline: A Forecasting Dilemma

The forecast of a potential global GDP decline due to climate change reveals the dire reality we may face if immediate action is not taken. With each 1°C increase in temperature, the associated economic impacts compound, culminating in significant losses that stretch far beyond mere productivity changes. These projections underscore the importance of integrating climate data and economic modeling to create accurate assessments that inform policymakers and stakeholders of potential economic futures.

In light of these findings, it is imperative for governments and organizations to reassess their economic strategies. The disconnect between typical economic growth metrics and the shrinking GDP associated with climate risks can create a false sense of security. Therefore, robust decarbonization policies and innovative approaches to carbon cost analysis are critical paths forward. By better understanding and addressing the combined threat of climate phenomena, we are more equipped to foster sustainable growth and resilience against the economic ramifications of climate change.

Decarbonization Policy: A Necessary Shift

As the research suggests, successful decarbonization can yield significant economic benefits. The social cost of carbon model indicates that transitioning toward greener practices can prevent substantial losses related to climate change. This model highlights that the economic viability of decarbonization strategies, especially in developed economies, far exceeds the costs typically associated with such interventions. By prioritizing environmental initiatives, countries can safeguard their economies while contributing to global efforts against climate change.

Investing in decarbonization not only aligns with environmental goals but also serves as a catalyst for job creation and innovation. Policies spawned from the 2022 Inflation Reduction Act, for example, have the potential to stimulate a green economy that counters the anticipated economic fallout of climate change. In essence, embracing robust decarbonization policies is fundamentally a proactive effort to reinforce economic resilience, improve energy independence, and mitigate the escalating costs associated with climate impacts, confirming that strategic investments in sustainability will indeed pay dividends.

The Cost of Carbon: Understanding Its Implications

The concept of the social cost of carbon plays a crucial role in discussions about climate change and economics. Recent findings revealed an updated estimate of $1,056 per ton of CO2 emissions, significantly higher than previous calculations. This discrepancy emphasizes the importance of recalibrating our approach to understanding the economic costs associated with carbon emissions and their far-reaching impacts. Framing the cost of carbon within our economic models can drive home the immediate need for effective climate action.

Adopting rigorous assessments of the social cost of carbon informs policymakers as they strategize for decarbonization efforts. By integrating this higher cost into economic planning, we can prioritize investments that mitigate climate change, with the added benefit of potentially stimulating economic growth through new green sectors. Understanding the financial realities tied to carbon emissions is vital for creating policies that address climate change while ensuring that economic gains coincide with ecological health.

Extreme Weather Events and Economic Resilience

Extreme weather events are becoming increasingly correlated with global temperature rise, leading to catastrophic impacts on economies worldwide. These phenomena can disrupt supply chains, damage infrastructure, and decrease productivity, compounding the economic costs of inaction. The variability of weather impacts across regions necessitates that policymakers ensure economic resilience is built into their climate strategies. Understanding these relationships enables governments to allocate resources towards adaptive measures that can combat the worst effects of climate disruptions.

As we continue to see shifts in climate patterns, the need for robust weather-related economic forecasts grows in importance. Investments in sustainable infrastructure not only provide immediate benefits but also serve as long-term safeguards against the escalating costs linked to extreme weather. Protecting economies from such disruptions requires a concerted effort to integrate climate projections into economic planning, thereby fostering resilience and ensuring stability in the face of a changing climate.

Long-term Economic Growth Amid Climate Challenges

While climate challenges loom large, long-term economic growth can still be envisioned with the right strategies in place. The nuanced findings from recent studies, which suggest growth may persist even under harsher climate conditions, indicate that resilience can be enhanced through proactive policies focused on sustainability. By addressing climate-related economic impacts now, nations can position themselves for a prosperous future, harnessing green technologies and investing in sustainable practices.

However, the trade-offs involved—such as the predicted 50 percent reduction in economic output if temperatures rise significantly—should spur immediate action. Rethinking economic frameworks to incorporate climate considerations allows for a more holistic understanding of potential futures. This integrated approach can illuminate pathways toward sustainable growth, ensuring that countries can thrive even as they navigate the complexities of a warming world and its economic reverberations.

The Role of Macroeconomists in Climate Strategies

Macroeconomists have a pivotal role in shaping how we understand and combat climate change implications on global economies. Through comprehensive studies and innovative modeling, they can accurately project the financial ramifications associated with temperature rise, shedding light on the urgent need for effective policy. As the recent research indicates, addressing the economic impact of climate change should become a central component of macroeconomic analysis and strategic planning.

By collaborating across disciplines and employing modern tools, macroeconomists can find solutions that balance economic growth with the pressing need for climate action. Their insights can influence critical decisions regarding investment in technology, infrastructure adaptation, and transitioning to renewable energy sources. In summary, the future often rests on the ability of macroeconomists to incorporate climate dynamics into economic forecasts, fostering a more resilient global economy.

Climate Change and Inequality: The Economic Divide

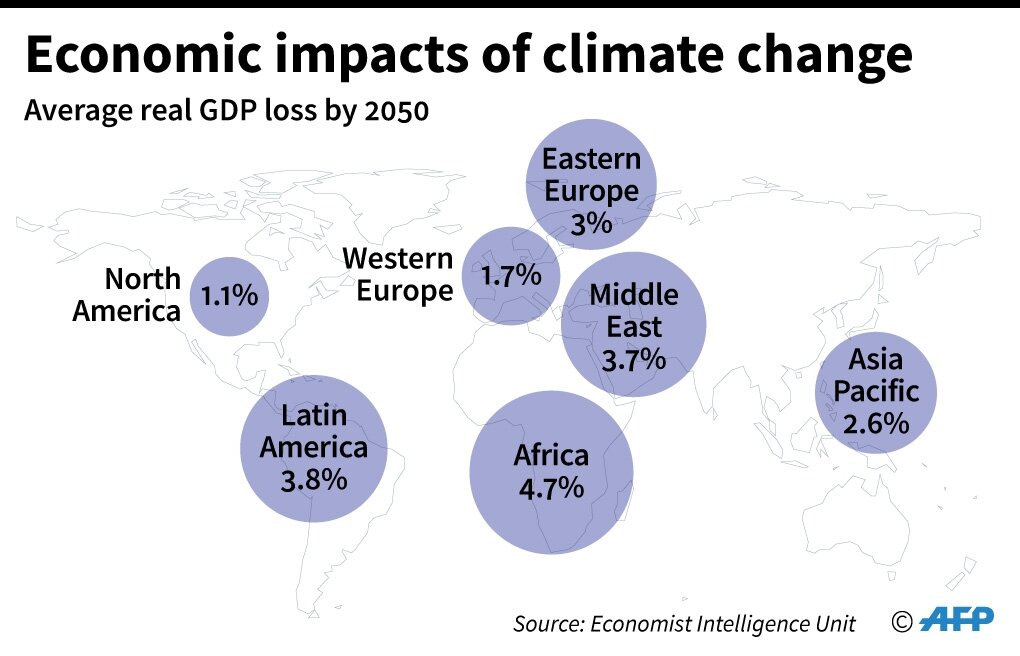

Climate change does not impact all nations equally; its economic repercussions often exacerbate existing inequalities. Vulnerable populations and developing nations face the largest risks, wherein the economic toll of climate change challenges their capacity to thrive. As temperature increases occur, these regions may suffer disproportionate losses in GDP, undermining any advancement made in terms of economic development. Addressing this inequality is essential for a holistic approach to climate change and economic stability.

To combat these disparities, it is crucial for international bodies to enact supportive policies that ensure equitable access to resources and technology for climate mitigation. Building adaptive infrastructure and promoting sustainable practices in these regions not only helps mitigate the impact of climate change but also fosters economic resilience. Bridging the economic divide while confronting climate change will require a concerted global effort centered around fairness and responsibility.

Frequently Asked Questions

How does climate change impact global GDP decline according to recent projections?

Recent studies suggest that each additional 1°C rise in global temperatures could lead to a 12 percent decline in global GDP. This projection highlights a more severe economic impact from climate change than previous estimates, indicating that the economic toll of climate change is much greater than once thought.

What are the economic implications of climate change projections for the future?

Climate change projections indicate that if global temperatures continue to rise, particularly by an additional 1-2°C, the economic implications could be catastrophic. For example, a 2°C rise could result in a 50 percent reduction in output and consumption over time, significantly affecting global economic stability and growth.

What is the estimated social cost of carbon related to the economic toll of climate change?

The social cost of carbon has been recalculated to be significantly higher than previous estimates, with the latest projections estimating it at around $1,056 per ton globally. This figure reflects the substantial economic toll of climate change and emphasizes the need for effective decarbonization policies.

How does decarbonization policy relate to the economic toll of climate change?

Decarbonization policies are essential to mitigating the economic toll of climate change. By investing in these strategies, economies can avoid significant GDP losses projected due to rising global temperatures. Recent analyses indicate that the cost of implementing decarbonization interventions is lower than the estimated social cost of carbon, suggesting a favorable cost-benefit scenario for major economies.

What are the challenges in assessing the economic impact of climate change?

Assessing the economic impact of climate change is complex due to various factors influencing productivity and emissions. Traditional models have often underestimated the effects of extreme weather events and the interplay between economic growth and temperature increases, leading to a disconnect between climate science and macroeconomic forecasts.

What does recent research say about the long-term effects of climate change on the economy?

Recent research indicates that while economies may still grow despite climate change, the potential for exponential losses in GDP suggests that the economic consequences could be long-lasting and severe. The findings emphasize that without addressing climate change, future economic growth may be significantly hampered.

Why do climate change projections predict economic consequences six times larger than earlier estimates?

New methodologies in climate change economics reveal that previous models underestimated the extent of GDP losses due to warming. The latest research has shown that each degree of temperature rise correlates with much greater economic damage than historically acknowledged, highlighting the urgency of addressing climate change.

| Key Points | Details |

|---|---|

| New Study Findings | Economic forecast projects a 12% decline in global GDP for each additional 1°C rise in temperature. |

| Comparison to Previous Estimates | The new findings indicate that the economic impact is six times larger than earlier estimates. |

| Methodology | The study utilized global temperature metrics over local variations and analyzed 173 countries. |

| Long-term Implications | A potential 2°C increase could result in a 50% reduction in output and consumption, surpassing the effects of the Great Depression. |

| Social Cost of Carbon | The study estimates the social cost of carbon at $1,056 per ton, significantly higher than previous estimates. |

| Decarbonization Benefits | The findings suggest that decarbonization policies are economically justified, particularly for large economies. |

Summary

The economic impact of climate change is profound and far-reaching, demanding immediate attention and action. Recent findings suggest that the rising global temperatures will result in significant economic losses, with projections stating that every additional 1°C could lead to a 12% decline in global GDP. This underlines the disconnect between climate science and macroeconomic predictions, emphasizing the need for a more integrated approach to assessing the financial ramifications of climate change. As the study shows, the long-term implications could be catastrophic, potentially reducing our economic output by half if global temperatures rise significantly. These findings highlight the urgent necessity for decarbonization strategies that can mitigate these risks and are economically viable.