The commercial real estate crisis is a pressing concern as vacancy rates soar and the market faces increasing challenges amidst rising interest rates. Since the pandemic, demand for office spaces in major U.S. cities has drastically declined, leading to a significant drop in property values and alarming financial analysts about potential bank failures. With an estimated twenty percent of the $4.7 trillion in commercial mortgage debt maturing soon, many lenders may find themselves in precarious situations if delinquencies rise. This scenario has sparked fears of a ripple effect on the broader U.S. economy, especially with high vacancy rates making it difficult for property funds to meet their financial obligations. As the landscape shifts, industry stakeholders are left questioning the stability of real estate loans and the future of commercial office investments in a post-pandemic world.

The ongoing turmoil in the commercial property sector is showing signs of a significant downturn that could reverberate throughout the financial system. As businesses continue to grapple with high office vacancy rates and the aftermath of shifting work models, the landscape for commercial real estate has become increasingly precarious. Experts are raising alarms about the potential for widespread bank troubles, citing the looming maturity of numerous real estate loans that could escalate into larger economic instability. With the struggle of numerous regional banks that heavily rely on commercial property investments, the question on everyone’s mind is whether these challenges could cascade into a more extensive financial disaster. Understanding the intricacies of this crisis is critical, as it holds the key to navigating its implications on both investors and the overall economy.

Assessing the Commercial Real Estate Crisis Impact

The ongoing commercial real estate crisis has raised alarms among economists as high vacancy rates plague major cities. With office spaces struggling to find tenants in the wake of the pandemic, the impact on the U.S. economy is palpable. Business leaders are increasingly cautious, and many are reconsidering their real estate investments. The Federal Reserve’s stance on interest rates complicates matters further, creating a perfect storm of high vacancy rates and unsustainable commercial real estate loans on the books of financial institutions.

Experts like Kenneth Rogoff emphasize that while significant banks appear resilient, the looming deadlines on real estate loans could pose substantial risks. When a large portion of commercial mortgage debt comes due, higher interest rates could prevent refinancing, leading to defaults. Such scenarios could trigger bank failures, particularly among smaller institutions that are less regulated. As these dynamics unfold, it becomes clear that the commercial real estate crisis is tightly interwoven with the broader health of the U.S. economy.

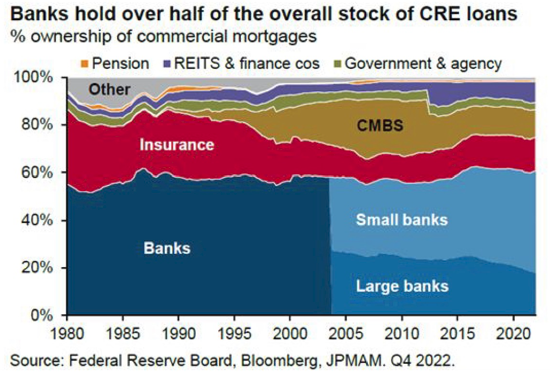

The Role of Bank Failures in the Real Estate Market

Bank failures can disrupt the commercial real estate market considerably as they lead to tighter lending conditions. If regional banks struggle with high delinquency rates on real estate loans, they may begin further restricting credit availability for borrowers. Without access to capital, many businesses could falter, leading to a downward spiral that ultimately impacts the job market and consumer spending.

Kenneth Rogoff points out that while small and medium banks might be at risk, larger institutions like Bank of America and JP Morgan have diversified portfolios that provide a buffer against such failures. Still, if a wave of defaults in commercial real estate occurs, even these larger banks could face significant challenges, affecting their stock performance and market confidence overall.

High Vacancy Rates and Their Economic Consequences

The high vacancy rates prevalent in major cities signal more than just empty buildings; they represent a shift in the work culture influenced by the pandemic. As companies embrace remote work, demand for traditional office space diminishes, leading to plummeting property values. This trend not only harms investors in the real estate market but also reverberates through the economy by reducing property tax revenues for cities.

Furthermore, these high vacancy rates may contribute to broader economic malaise. With office spaces stagnant, local businesses such as cafes and retail shops that relied on foot traffic could also suffer, leading to job losses and decreased consumer spending. The cyclical effect of high vacancy rates showcases the interconnected nature of real estate and the overall economic landscape.

Interest Rates: A Critical Factor in the Real Estate Crisis

Interest rates remain a decisive factor in the commercial real estate crisis, influencing borrowing costs and investment strategies. High interest rates have been a double-edged sword; while they are generating profits for banks, they complicate refinancing options for property owners facing maturing loans. Many investors who over-leveraged during periods of low rates now find themselves in precarious positions.

As interest rates rise, the appetite for real estate loans diminishes, causing a cascading effect where banks may struggle to offload these assets. Kenneth Rogoff points out that many analysts believe that if long-term interest rates were to fall, it would provide relief for property owners and potentially stabilize the market. However, the prevailing opinion is that such a shift is unlikely without a major economic downturn.

Exploring Solutions to Avert Real Estate Collapse

The question of whether anything can be done to avert a collapse in the commercial real estate market is contentious. Despite the looming crisis, experts such as Rogoff emphasize the importance of systemic resilience fostered through regulatory measures post-2008. However, small banks, not facing the same stringent guidelines, could find themselves vulnerable if they are unable to adapt to the changing landscape.

While conversations around potential bankruptcies are alarming, they are particularly significant for the local economies they serve. Addressing these challenges will require a multifaceted approach that considers both the need for updated regulations and the economic realities facing real estate owners. Long-term strategies may include policy adjustments or financial incentives aimed at stimulating demand for commercial properties.

Economic Repercussions of Commercial Real Estate Defaults

Defaults on commercial real estate loans could lead to broader economic repercussions that extend far beyond the banking sector. As regional banks face losses, the potential for stricter lending practices could stifle business growth and consumer confidence. If large portions of the banking system become embroiled in bad debt, the stakes of these issues signal a need for close monitoring and intervention.

Furthermore, the correlation between commercial property losses and consumer wealth is notable, particularly through pension fund implications. If pension funds experience significant losses due to failing real estate investments, the ensuing reduction in disposable income could further curtail consumer spending, stunting economic growth even in an otherwise stable environment.

Examining the Shifting Dynamics of Commercial Property Demand

The pandemic redefined the demand for commercial property, compelling business executives to rethink their office space needs. Many companies now prefer a hybrid workforce model, leading to increased vacancies and reduced demand for traditional office spaces. This structural shift sparks concerns over the viability of certain types of commercial investments, with many investors questioning the future profitability of office buildings.

While some market segments like premium properties are seeing resilience, the broader picture shows a declining interest in traditional office real estate. Investors and stakeholders must adapt to these changing circumstances or face the reality of stagnant or declining investment returns. Strategies such as converting commercial spaces to residential use may provide some solutions, but the challenges posed by zoning laws and structural limitations must be addressed.

The Interaction of the U.S. Economy and Real Estate Sector

The U.S. economy’s health is inherently tied to the real estate sector, making the current commercial real estate crisis particularly concerning. A thriving market is essential for driving economic growth, job creation, and consumer spending. However, with the rising number of delinquent loans likely to impact bank stability and, subsequently, the economy, the stakes are high, and observers remain vigilant.

Despite fears of a massive downturn, the economy is currently bolstered by a robust labor market and strong consumer spending, proving that not all sectors are equally vulnerable. Economists caution, however, that if the real estate market were to experience a severe contraction, it could quickly ripple across the economy, affecting everything from consumer confidence to job security.

Navigating the Future of Commercial Investments

As the commercial real estate landscape evolves, stakeholders must navigate a path filled with uncertainties and potential pitfalls. Understanding the implications of bank failures and high vacancy rates is essential for real estate investors and financial institutions alike. Those who can anticipate market trends and adjust strategies accordingly may stand to benefit in an otherwise tumultuous economic environment.

Efforts to revive the real estate sector may involve collaborative approaches among public and private entities. By engaging in adaptive strategies and innovative financing methods, stakeholders can work towards stabilizing the market. Ultimately, navigating the future of commercial investments will require vigilance and flexibility as industry trends continue to unfold.

Frequently Asked Questions

How is the commercial real estate crisis impacting bank failures in the U.S. economy?

The commercial real estate crisis is leading to fears of increased bank failures due to high vacancy rates and upcoming delinquent real estate loans. Many regional banks have significant investments in commercial properties that are losing value as demand diminishes. This scenario could result in widespread losses for these banks if borrowers default on loans, heightening the risk of failures among smaller financial institutions while larger banks, better capitalized, are less affected.

What are the causes behind the high vacancy rates in commercial real estate?

High vacancy rates in commercial real estate are primarily due to the shift in work habits brought about by the COVID-19 pandemic. Many businesses have embraced remote or hybrid work models, resulting in a reduced demand for office space. As of now, vacancy rates in some U.S. cities range from 12 percent to 23 percent, which is putting downward pressure on property values and leading to a broader economic impact.

What potential effects could the commercial real estate crisis have on real estate loans?

As commercial real estate values drop, there is a growing risk of delinquencies on real estate loans coming due, particularly with 20% of commercial mortgage debt maturing this year. This situation raises alarms as lenders could face significant losses, affecting the availability of future loans and potentially tightening lending conditions across the financial sector.

How are interest rates linked to the commercial real estate crisis?

Rising interest rates have exacerbated the commercial real estate crisis by increasing borrowing costs for businesses and property developers. Many investors had previously assumed low interest rates would persist, leading to over-leveraging in the market. As financing becomes more expensive, it becomes challenging for property owners to refinance, perpetuating high vacancy rates and declining property values.

Could the commercial real estate crisis lead to a broader economic downturn?

While the commercial real estate crisis is serious, experts suggest it may not trigger a full-blown financial crisis akin to 2008. Elevated vacancy rates and potential bank losses could lead to regional economic distress, lower consumer spending, and stricter lending practices. However, the overall U.S. economy is currently buoyed by a strong job market and thriving stock market, which may cushion some of the impacts of this crisis.

What measures can be taken to address the challenges in commercial real estate?

To mitigate the commercial real estate crisis, a reduction in long-term interest rates could help stabilize refinancing for property owners. Additionally, restructuring distressed loans and incentivizing adaptive reuse of vacant properties into mixed-use developments may create new opportunities. However, these solutions face challenges, particularly around regulatory and zoning issues.

What is the outlook for the U.S. economy amidst the commercial real estate crisis?

The outlook for the U.S. economy remains mixed despite the commercial real estate crisis. While high vacancy rates and rising interest rates pose challenges for certain sectors, the economy as a whole is benefiting from a robust job market and stock performance. The real estate sector’s struggles could impact regional banks and contribute to tighter lending, but significant economic growth is still anticipated barring any unforeseen downturns.

Which banks are at risk due to the commercial real estate crisis?

Regional banks, which have significantly invested in commercial real estate, are particularly vulnerable to the crisis as many face weaker capital positions. Unlike larger banks that are more diversified and better capitalized, smaller banks could experience heightened risks of defaults on commercial real estate loans, which could lead to more bank failures if not managed appropriately.

| Key Points | Details |

|---|---|

| High Office Vacancy Rates | Office vacancy rates have surged post-pandemic, reaching 12% to 23% in major U.S. cities, which is affecting property values. |

| Potential Economic Impact | Experts worry about potential widespread bank losses due to upcoming commercial real estate loan maturities, but a financial meltdown is not expected. |

| Commercial Real Estate Debt Due | 20% of the $4.7 trillion commercial mortgage debt is expiring this year, which could affect banks, especially smaller ones. |

| Market Optimism vs Risks | Some investors maintain optimism about long-term interest rates declining, but the current economic conditions remain challenging. |

| Differences with 2008 Crisis | While losses are expected, the situation is not anticipated to mirror the financial crisis of 2008 due to stricter regulations on banks. |

| Bank Vulnerability | Smaller banks face more risk due to less stringent capital requirements and previous struggles with rising interest rates. |

| Overall Economic Resilience | Despite commercial real estate challenges, the broader economy is stable due to strong job and stock market performance. |

Summary

The commercial real estate crisis is a pressing concern that is expected to unfold over the next couple of years due to high vacancy rates and looming debt obligations. As companies continue to reduce their office spaces in the aftermath of the pandemic, financial experts warn that significant losses in this sector could ripple through the banking system, particularly impacting smaller institutions. However, while challenges abound, many economists believe that we are currently witnessing a constrained impact on the broader economy, given the robust job market and ongoing financial stability.